The increase in the federal interest rate is the topic du jour. But what does this mean in real terms for the average home buyer and the home market in general?

The US Federal Reserve or ‘the Fed’ is the central bank which loans money to banks and sets the interest rate based on the state of the national economy. Increasing the interest rate discourages spending and keeps the costs of goods and services lower by decreasing demand. An increase in interest rates encourages borrowing and spending which generally stimulates growth.

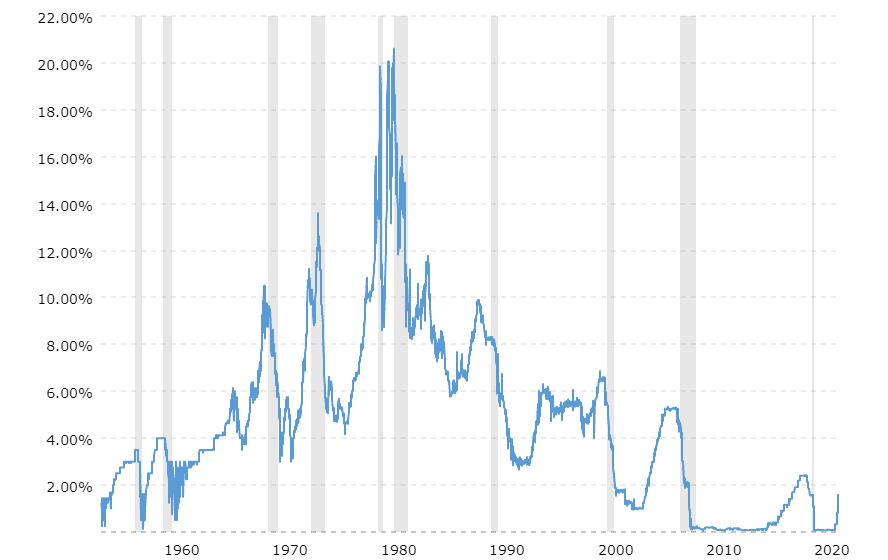

Interest rates have fluctuated between near zero and highs of over 20 in the last 60 years. Check out the graph below for the context of current federal interest rates.

Federal interest rates directly influence mortgage lender rates. When federal interest rates go up, mortgage lenders increase the rates for their products. Some home loan packages are less impacted by the federal interest rates because they are directly subsidized by the federal government. For instance veteran home loans or first time home-buyer loans have lower rates than conventional loans.

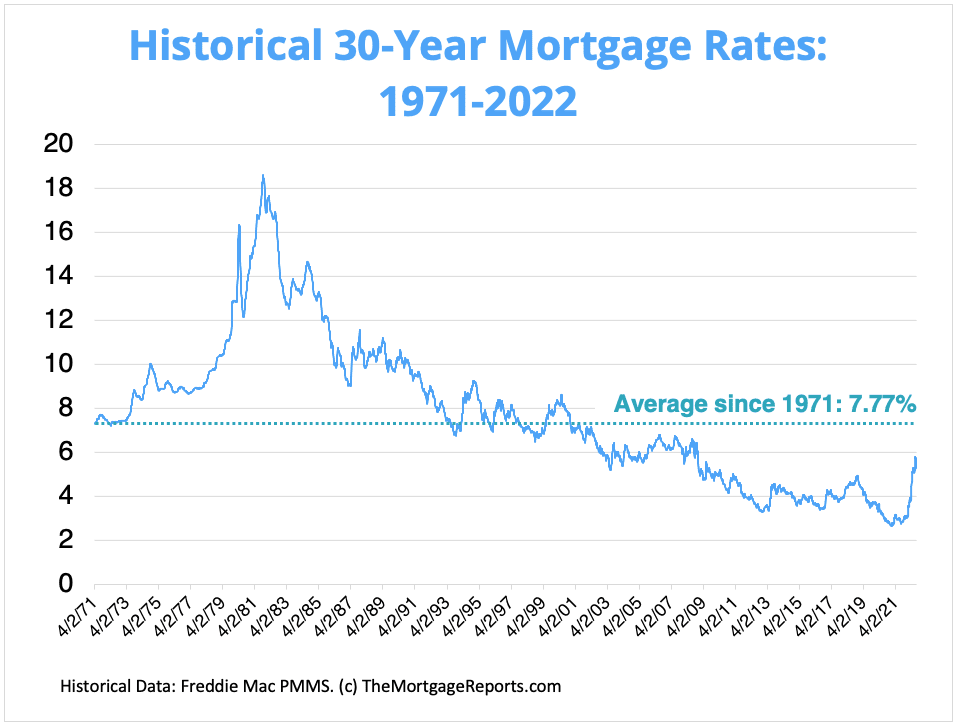

Compare the above chart with the chart below of average mortgage rates since the 1970’s.

As you can see, mortgage rates and Federal Interest rates are siblings but not twins. This is because mortgage lenders have flexibility to adjust their rates based on the Federal Interest rates, their customer base, and the market.

Mortgage lenders also have an interest in keeping their rates less volatile than Federal Interest rates to prevent shock.

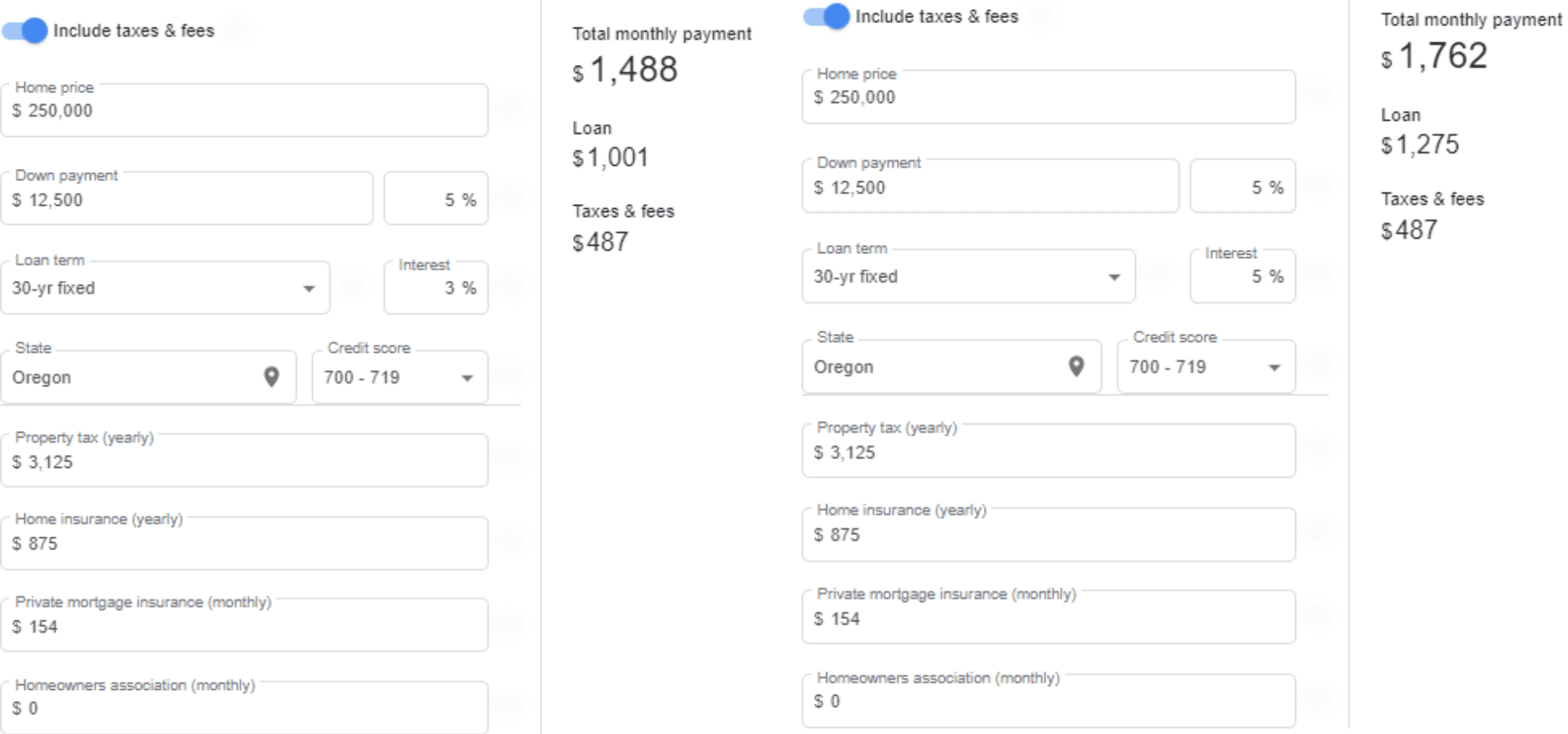

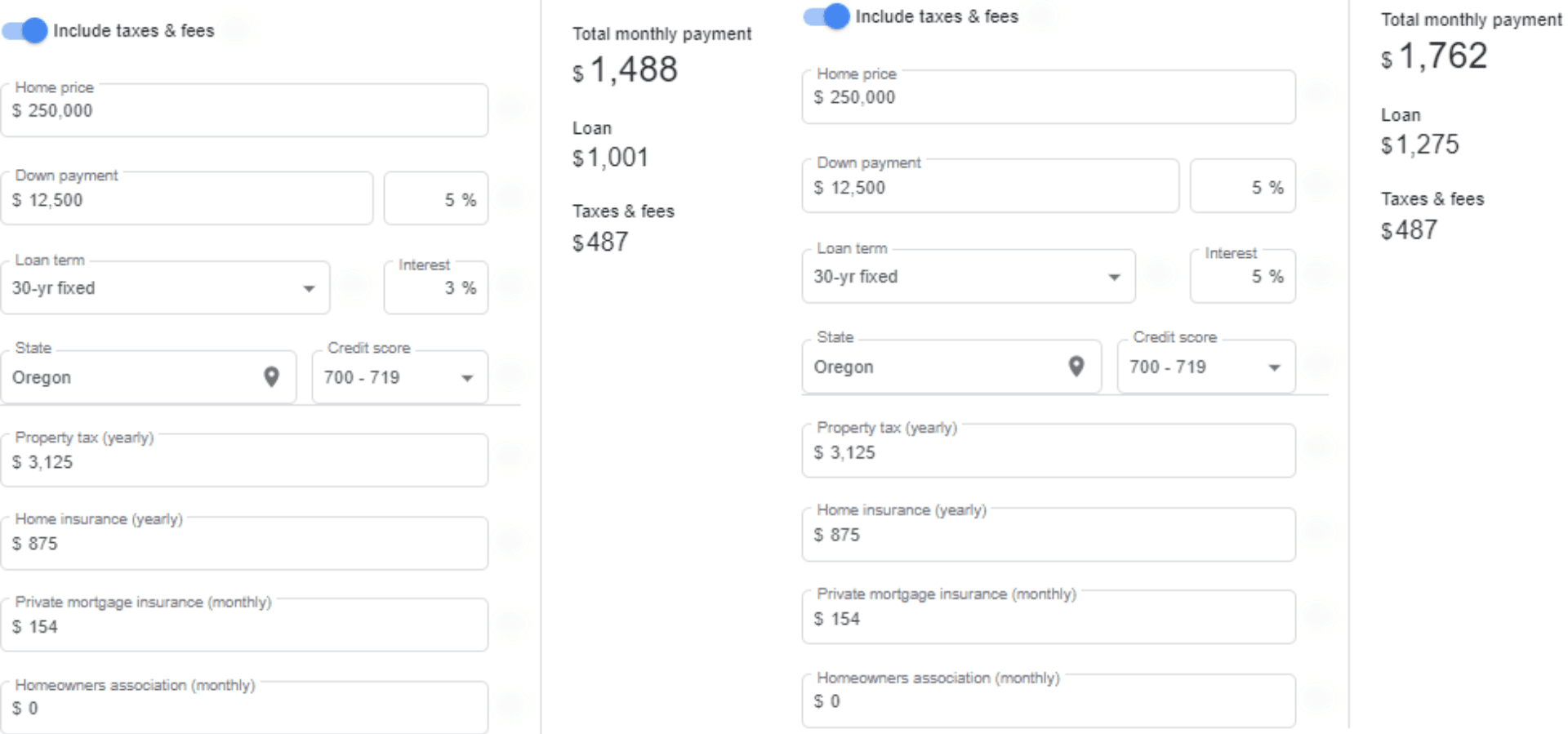

Let’s look at the difference between a 3% and a 5% interest rate for a conventional 30 year loan with 5% down on a $250,000 home. As you can see from the charts below the monthly payment difference between a 3% and 5% loan is over $200 per month, which almost doubles when looking at a 6% rate. For a homeowner to afford the monthly payment, they will need to have a better income to debt ratio as well as more for down payment.

This could potentially be a great thing for middle income buyers. Even though the interest rates are higher which increases the cost of the loan, there are fewer buyers which means fewer bidding wars. In Beaverton for instance this could knock off an additional $50,000 from the final price of the home!

Let's say you're looking at a $450,000 home at 3.5% with 10% down, you have a loan balance of $405,000. At the 3.5% rate, your monthly payments would be $1819. At 5.75%, today's rates, the same payment would now be $2363, an increase of $545 monthly of $6,538 annually. Here's the advantage, up until the end of May 2022, buyers were bidding anywhere from $20,000 to $80,000 more than asking. By not having to bid $20,000-$50,000 over you'll make up the difference in 4-8 years.